When it comes to small business accounting, there’s a lot you need to know in order to make the most informed financial decisions. One of the best places to start is to understand the calculation of key financial ratios and their interpretation. Before we dive into the key ratios, let’s do a quick refresher on three key financial statements: the balance sheet, income statement and statement of cash flow.

KEY FINANCIAL STATEMENTS

THE BALANCE SHEET

The balance sheet provides a look at your company’s financial position at a specific point in time. This financial statement is made up of three components: assets, liabilities and shareholders' equity. The assets include anything the company owns such as cash, equipment, property or inventory. Liabilities include accounts payable or any type of payment made on a long-term loan. The owners' or shareholders' equity refers to what’s leftover after the amount of liabilities is subtracted from the amount of assets.

Assets are listed on the left side of the balance sheet. Liabilities and equity are listed on the right side.

The reason it's called a balance sheet is because of the formula:

Assets = Liabilities + Shareholders' Equity

THE INCOME STATEMENT

As the name suggests, the income statement outlines your profitability over a period of time such as a month, quarter or year. It’s also known as the profit and loss (P&L) statement and contains the following components:

- Sales encompasses total revenue generated as well as the cost of all goods sold.

- Operating expenses include items such as advertising and rent for office space.

- Non-operating expenses can include a one-time purchase and interest on any debt taken on by the company.

STATEMENT OF CASH FLOW

A cash flow statement provides a picture of where a company's cash inflows and outflows. Analyzing your cash position and anticipating your cash flow needs are extremely important small business accounting tasks that must be done on a regular basis.

Remember, cash is king. Your business could be recording a profit each quarter but may be experiencing a cash crisis because you are having a tough time converting assets such as accounts receivables into cash. You need cash to pay things like salaries and rent. Unfortunately, you can’t pay in “profit.”

RELATED: How to Forecast Cash Flow in QuickBooks

CREATING A CHART OF ACCOUNTS

The Chart of Accounts offers an excellent a way to record all of your transactions for income, expenses, or liabilities. If you earn money it will be recorded in an income account. If you buy business supplies, that transaction will be recorded in an expense account. There’s even an account for liabilities such as mortgages or loans.

QuickBooks helps simplify this small business accounting task. You can access the Chart of Accounts window in one of three ways:

- Press Ctrl+A (this can be done from any page in the program)

- In the menu bar, choose Lists →Chart of Accounts

- At the top right of the Home Page, in the Company panel, click Chart of Accounts

Once the Chart of Accounts has been opened you can create new accounts.

- Press Ctrl+N to open the Add New Account window. On the menu bar at the bottom of the Chart of Accounts window, click Account →New. Or right click anywhere in the Chart of Accounts window, then choose New from the shortcut menu. Either method will prompt QuickBooks to open the Add New Account window.

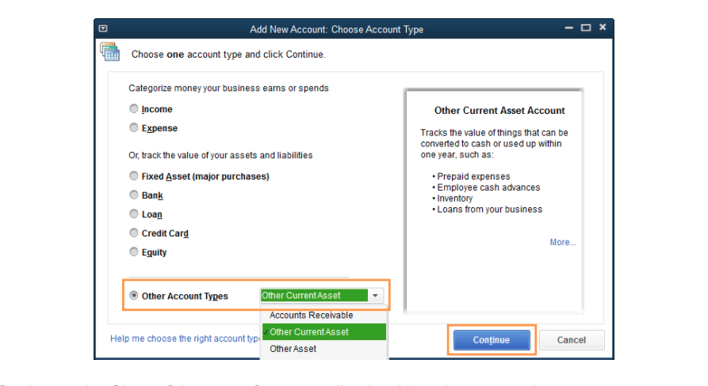

- Select the type of Account you want to create, such as Bank for a bank account, and then click Continue. The Add New account window lists the most common kinds of accounts. If you don’t see the account type you want, then select the Other Account Types option and then choose from the drop-down menu shown below.

FINANCIAL RATIOS

Now that we have a good understanding of the key financial statements and how to track transactions, it’s time to take a look at financial ratios. There are several different types of financial ratios but in this post, we’ll be looking at two categories: profitability and liquidity. Understanding these will offer a good starting point to evaluating the financial health of your business.

PROFITABILITY RATIOS

|

SAMPLE INCOME STATEMENT HealthMax Inc |

|

|

for the quarter ended March 31, 2017 |

|

|

Sales |

|

|

Blender Bottles |

100,000 |

|

Multi Vitamin Mix |

150,000 |

|

Total Sales |

250,000 |

|

Cost of Good Sold |

|

|

Blender Bottles |

17,500 |

|

Multi Vitamin Mix |

10,000 |

|

Total Cost of Goods Sold |

27,500 |

|

Gross Profit |

222,500 |

|

Operating Expenses |

|

|

Salaries |

19,500 |

|

Rent |

5,000 |

|

Utilities |

500 |

|

Total Operating Expenses |

25,000 |

|

Non Operating Expenses |

|

|

Interest |

7,000 |

|

Taxes |

1,000 |

|

Total Operating Expenses |

8,000 |

|

Net Income |

189,500 |

Gross Margin

Gross margin is a percentage that you can calculate by looking at your income statement. This percentage tells you how much money you get to keep from your sales after you pay for the costs you incurred to make your product or provide your service.

The equation for finding your gross margin is:

Gross Margin % = (Revenue - Cost of Goods Sold) / Revenue

For example, let’s say you generated sales of sales of $250,000 and your cost of goods sold was $27,500. This means your Gross Profit is $222,500 ($250,000 - 27,500) and your Gross Margin is 89% ($222,500 / $250,000).

In other words, for every $1 that you make selling your product, you get to keep 89 cents to run your business.

RELATED: How to Calculate Gross Margin for Your Business

Break-even point

The break-even point is the amount of sales you need to generate just to produce a profit of zero. It’s the amount you need to earn in order to stay in business. Here is the formula:

Break-even Point = (Overhead Expenses + Balance Sheet Payments) / Gross Margin

Your overhead expenses refer to costs that you incur regardless of how many blender bottles you sell in a particular quarter (using our example company above). Examples include salaries, utilities, insurance and rent. In order to calculate the break-even point, you will also need to know the total balance sheet payments such as interest expense on loans.

Armed with this information, your break-even point is calculated as ($25,000 + $7,000) / 0.89 = $35, 955.

That means in order for your business to stay in operation, you must generate revenue of $35,955. This number should be used as a yardstick or benchmark in evaluating business performance. Think of it as the bare minimum you need to achieve in order to keep the doors open.

RELATED: How to Calculate Your Break-Even Point

Net profit margin

This ratio takes a look at the amount of net income earned with every dollar of sales the company generated. The calculation is below:

Net Profit Margin = Net Income / Revenue

- Hint: Net Income is calculated as Revenue - Cost of Goods Sold - Total Operating Expenses - Interest Expense - Taxes

Using the data above, your net profit margin would be $189,500 / $250,000 = 76%. This means for every dollar in sales, the business profits 76 cents.

For the remaining two profitability ratios, we will need to incorporate line items from the balance sheet as well as the income statement.

|

SAMPLE BALANCE SHEET |

||||

|

as at March 31, 2017 |

||||

|

ASSETS |

$ |

LIABILITIES |

$ |

|

|

Current Assets |

Current Liabilities |

|||

|

Cash |

50,000 |

Accounts Payables |

50,500 |

|

|

Accounts Receivable |

100,000 |

Accrued Liabilities |

10,000 |

|

|

Inventory |

100,000 |

Accrued Taxes |

10,000 |

|

|

Total Current Assets |

250,000 |

Total Current Liabilities |

70,500 |

|

|

Property Plant & Equipment |

Long-Term Liabilities |

|||

|

Land |

100,000 |

Notes Payable |

69,000 |

|

|

Total Property Plant & Equipment |

100,000 |

|||

|

TOTAL LIABILITIES |

139,500 |

|||

|

TOTAL ASSETS |

350,000 |

|||

|

EQUITY |

||||

|

Common Stock |

200,000 |

|||

|

Retained Earnings |

100,000 |

|||

|

Less: Dividends Paid |

89,500 |

|||

|

TOTAL EQUITY |

210,500 |

|||

Return on Assets (ROA)

This calculation tells us how well management used the company’s assets to generate profit and is calculated as follows:

Return on Assets = Net Income / Total Assets

Using this formula, your ROA would be $189,500 / $350,000 = 0.54 or 54%.

Return on Equity (ROE)

This calculation measures how much profit the company generated using the money invested by shareholders.

Return on Equity = Net Income / Shareholder's Equity

The ROE for our sample company would be $189,500 / $210,500 = 0.90 or 90%.

LIQUIDITY RATIOS

Working Capital

Working capital is a popular measure of short-term liquidity. It is calculated as follows.

Working Capital = Current Assets - Current Liabilities

As a refresher, current assets refer to assets that are expected to convert into cash within a year and include things like accounts receivable and inventory. On the other hand, current liabilities refer to obligations which are coming due within a year such as accounts payable.

Using our example balance sheet above, the company’s working capital is $179,500 ($250,000 - $70,500).

This is a good indicator of financial strength. If the company had negative working capital, it could signal bad news such as impending bankruptcy.

Current Ratio

This metric uses the same components as working capital but presents the information as a ratio. Here is the formula:

Current assets / current liabilities

Using the example above, your current ratio would 3.55 ($250,000 / $70,500) meaning that your business has 3.55 times more current assets than it does current liabilities. In general, a ratio of 2:1 is considered to be healthy because it indicates the company can more easily satisfy its current financial obligations. At the same time, if the current ratio is too high (relative to past performance or industry trends) then it could mean that you need to manage your working capital better.

Quick Ratio

Also known as the “acid-test ratio" or "quick assets ratio," this metric tells us how well a company can meet its current liabilities using its most liquid assets. This is precisely why the quick ratio excludes inventory from the calculation since it is often harder to convert to cash. Here is the formula:

Quick ratio = (current assets - inventory) / current liabilities

Our quick ratio would be ($250,000 - $100,000) / $70,500 = 2.13. This is a big difference compared to our current ratio results above.

PUTTING IT ALL TOGETHER

As you can see, the calculation of financial ratios is not difficult. It’s a matter of knowing what data to pull and computing your formulas. However, it’s important to know that on their own, financial ratios don’t tell you much.

Going back to our very first calculation above, we found that the company’s gross margin is 89%. But, is that good or bad? The first step is taking a look at how this measure has been trending quarter over quarter and year to year.

However, to have a full view of your business performance you must remember that your business does not operate in a vacuum. Therefore, it is critical to take into account industry data as well when it comes to analyzing your results. For instance, if your quick ratio is increased from 1.8 to 2.13 compared to the previous year, but the industry standard happens to be 3, then it means you’ve got some work to do.

It is also worth mentioning that lenders use these small business accounting metrics along with liquidity ratios by to assess how likely a business would be to default on a loan. Knowing how to calculate and measure ratios is one thing. Working to improve your financial performance is another.

NEXT STEPS

At this point, it may be helpful to get some professional help to assist with your small business accounting needs. Hiring your own in-house accountant can get extremely costly. However, outsourcing your accounting and bookkeeping to a firm like Ignite Spot saves you time and money, allowing you to focus on your core operations. With outsourced accounting from Ignite Spot, you won't have to worry about the principles of accounting; you have enough to worry about just running your business.

More specifically, our CFO services, will help you to unlock invaluable financial insights in order to streamline operations, improve cash flow management and make the best decisions to take your company to the next level of success. Click here to book your first CFO session, for free.

.webp?width=300&height=67&name=image%20(4).webp)

.webp?width=160&height=160&name=Gold%20(1).webp)